Select a different country or region to view content tailored to your location.

Alison Heyerdahl is the Head of Content at FxScouts, a Chartered Market Technician (CMT), and an experienced trader, as well as a financial writer with extensive expertise in Forex trading, broker analysis, and market research. She has reviewed 100+ brokers, publishes weekly YouTube trading videos, and co-hosts the “Let’s Talk Forex” podcast.

Starting your Forex trading journey in South Africa requires understanding the basics of regulation to ensure a safe trading environment. It's crucial to trade only with brokers regulated by the Financial Sector Conduct Authority (FSCA) or other reputable international regulatory bodies.

This guide will help you understand why regulation is important, how to check whether your broker is regulated, the signs of potentially unsafe brokers, and additional critical information for secure trading.

Forex and CFD trading involves significant financial risk, so regulation is vital for your protection. In South Africa, the FSCA monitors brokers to ensure they operate transparently and fairly. Here’s how regulation benefits you:

Without regulation, traders face risks like manipulated trades, hidden fees, and difficulty withdrawing funds.

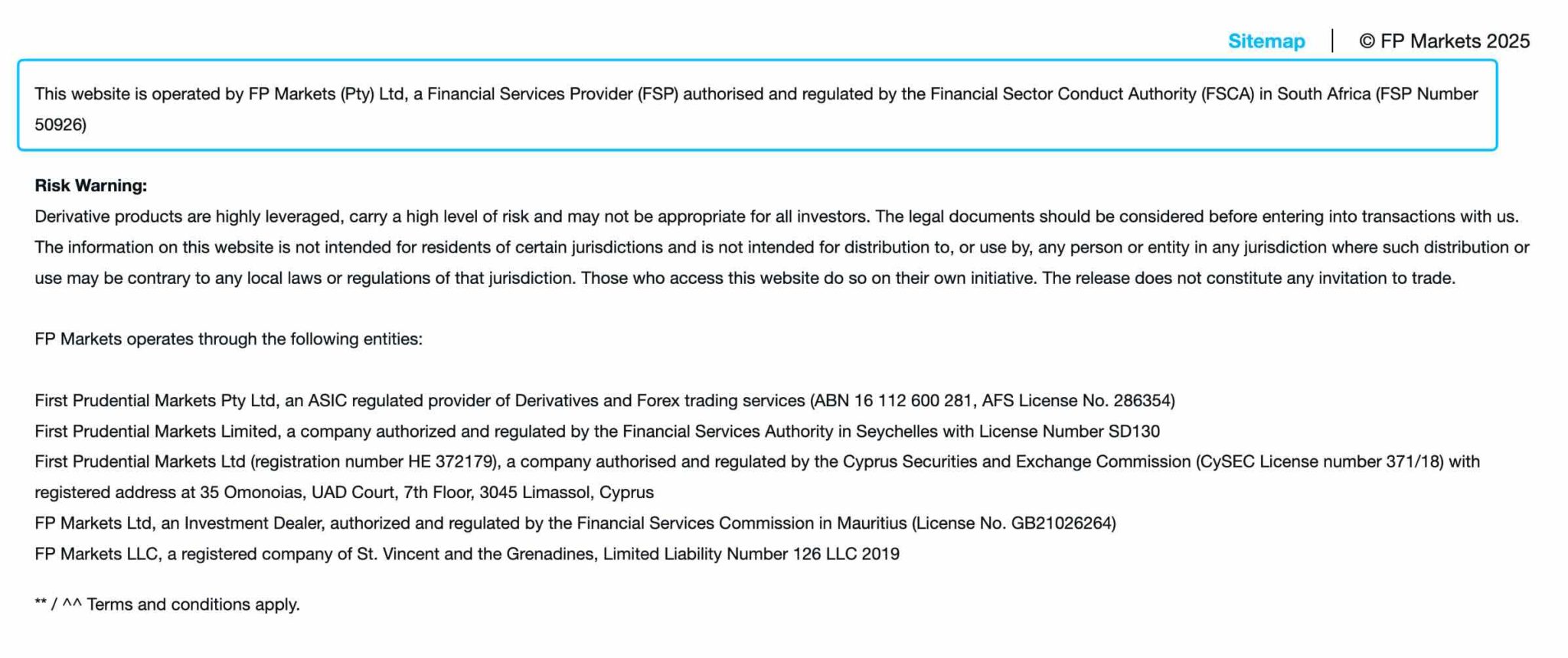

The Financial Sector Conduct Authority (FSCA) is the main regulator overseeing Forex trading in South Africa. Established in 2018 under the Financial Sector Regulation Act, the FSCA replaced the Financial Services Board (FSB) and ensures all financial services providers, including Forex brokers, comply with regulations.

Brokers licensed by the FSCA are known as Financial Services Providers (FSPs) and must meet strict financial and operational standards. Non-compliant brokers face penalties, license suspension, or even permanent revocation.

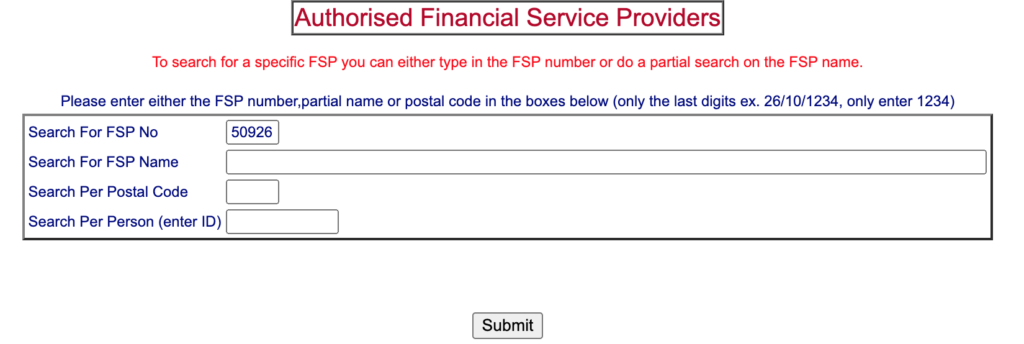

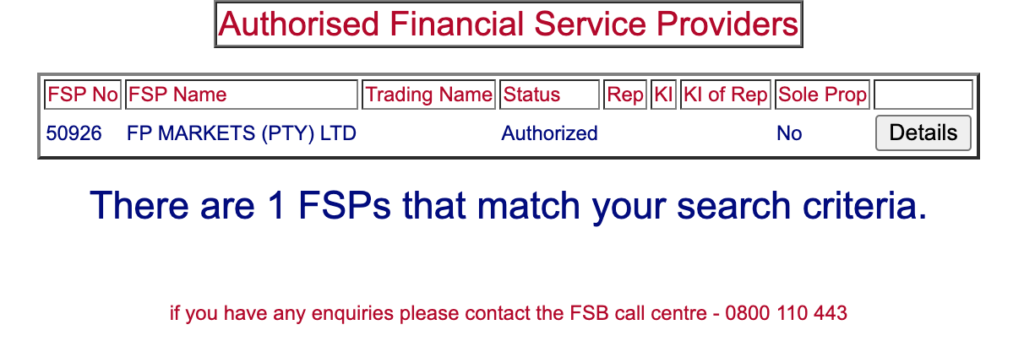

Verifying a broker’s FSCA license is straightforward and essential. Here's how:

Any discrepancies or missing information should be considered a red flag. Watch this video to learn more on how to determine if your broker is FSCA regulated.

Unregulated brokers pose significant risks. Watch out for these warning signs:

If you have an issue with an FSCA-regulated broker, you can lodge a complaint directly with the FSCA. Typically, disputes are reviewed, and decisions are provided within a reasonable timeframe. Visit the FSCA’s website to submit a complaint and find additional resources.

The FSCA mandates brokers to maintain strict standards, but it does not provide a specific investor compensation scheme like some international regulators (e.g., FCA in the UK). Consider brokers with multiple licenses to benefit from international investor protection schemes.

Before opening an account, always ask brokers:

The FSCA encourages responsible trading and robust risk management practices. Although the FSCA does not set specific leverage limits, it emphasises that traders should carefully select brokers who clearly outline leverage and margin requirements and provide adequate educational resources for managing risk. Traders should confirm the leverage options directly with their FSCA-regulated brokers.

While FSCA regulation is vital, brokers regulated by reputable international bodies add extra protection. Trusted global regulators include:

Choosing brokers with multiple regulatory licenses can provide enhanced security.

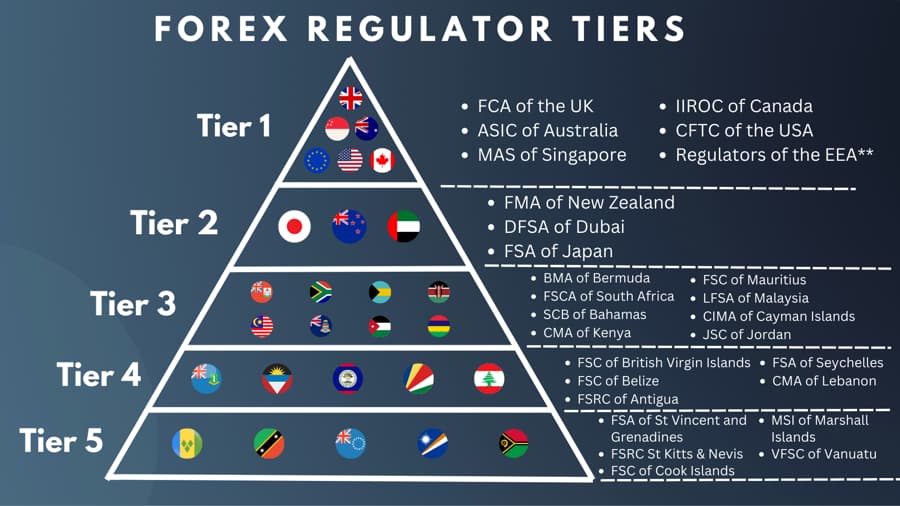

Below is a depiction of the various regulators and their jurisdictions. Regulators at the top of the triangle are the world’s top regulators, while those at the bottom provide virtually no regulatory oversight.

**Regulators of the EEA in alphabetical order:

We consider numerous factors when deciding which tier a regulator belongs to.

Rules and Regulations: These are the legal obligations regulators place on brokers and other financial services companies. For example, all regulators require brokers to segregate their operating capital from their clients’ trading funds to prevent client losses in the event of broker bankruptcy. Tier 1 regulators, like the FCA or CySEC (of Cyprus in the EU), also require brokers to limit the leverage they offer and provide all their clients with negative balance protection. Most regulators in Tier 2 and below have more relaxed leverage limits or do not require negative balance protection. Those in Tier 4 and below either have very few rules for brokers or none at all. The organisations in Tier 5 are not regulators at all, they allow any financial company to register within their jurisdiction but do not provide any oversight or management.

Enforcement: How well a regulator enforces rules and regulations is equally important. There is no point in regulators requiring brokers to treat traders fairly if they don’t follow up on complaints, conduct audits and carry out surprise on-site visits. This is where some regulators struggle. Most of the Tier 3 and 4 regulators are well-intentioned but fail to enforce their rules consistently. All Tier 1 regulators are proactive, strict and ruthless when enforcing regulations.

Consumer Protection: A central pillar for all regulators is protecting consumers. This includes education and outreach, working closely with brokers to ensure that an appropriate level of due diligence is carried out on clients, passing on valid complaints to the financial ombudsman for arbitration, and taking rule-breakers to court and removing their licences to operate.

There are many other less strict regulators around the world, and Forex brokers will hold licences with them to avoid the restrictions placed on them by ASIC, CySEC and the FCA. These regulators are often based in small island states and are known as “offshore” regulators.

Common offshore regulators include the Seychelles FSA, the Mauritius FSC, the St Vincent and Grenadines FSA, the Belize IFSC and the Bahamas SCB. While being regulated by one of these smaller regulators does not mean that a broker is bad, it does mean that traders are not as well protected.

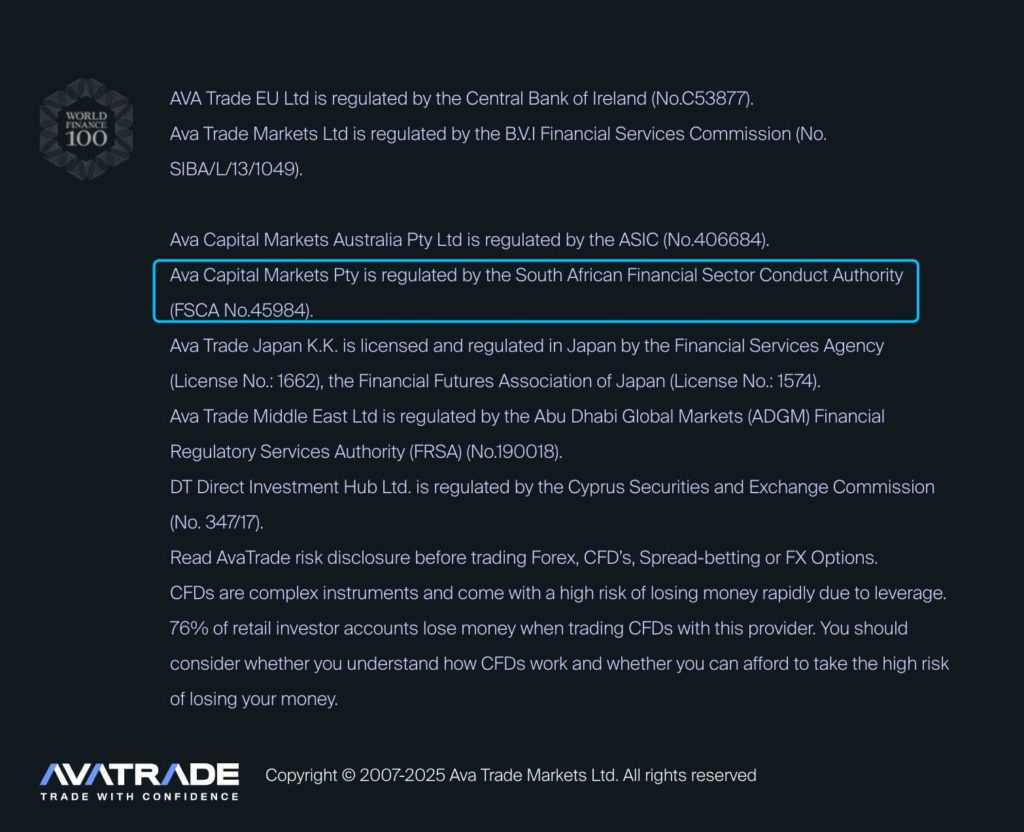

The best and most trustworthy brokers are regulated by at least one of the three major regulators (FCA, CySEC, ASIC) or the FSCA. It is common for brokers to have multiple regulators, one for each region in which they operate. A good example of this is Avatrade. Below is a screenshot from the bottom of their website:

We can see that ASIC, CySEC, the FSCA, Financial Services Agency of Japan, FRSA, and B.V.I regulate AvaTrade and its subsidiary companies. Traders will, therefore, register an account with the relevant subsidiary based on their country of residence. For example, traders in South Africa will be onboarded through the subsidiary regulated by the FSCA, while Australian residents will be onboarded through the ASIC-regulated entity.

If you have been the victim of a scam, you should always contact your local regulator to make a complaint. In South Africa, you can contact the FSCA here, and you can contact the FAIS Ombudsman here. If your complaint concerns an offshore broker, contact the relevant financial regulator in that region. Although they may not be able to retrieve your money, financial regulators will become aware of these brokers and can take action against them.

We also collect information on scam brokers. Please inform us of any fraudulent activity you have encountered by filling out the scam broker report. Also, check out our broker trust checker tool to help you validate the trustworthiness of a broker.

Watch our video on how to spot a scam broker:

Trading with a regulated Forex broker ensures better protection for your funds and a safer trading experience. Always verify FSCA licenses before making deposits and stay alert to potential scams.

By following these guidelines, you can confidently begin your trading journey in South Africa.

Also check out our guide to the top FSCA-regulated Forex Brokers in South Africa!

Explore more resources that fellow traders find helpful! Check out these other guides to enhance your forex trading knowledge and skills. Whether you’re searching for the best brokers, educational material, or something more specific, we’ve got you covered.

Compare the best Forex trading platforms for 2026, including MT4, MT5, cTrader, and TradingView. Find the right tools to enhance your trading experience.

What is Forex trading and how does it work? An easy-to-read guide including how to trade, and how to choose a reliable broker.

Compare FSCA-regulated forex brokers in South Africa by ZAR accounts, local deposit methods, withdrawal speed, spreads, and platform support. Independently tested for South African traders.

Partner Manager and Financial Writer

Head of Content

Financial Writer